TL;DR:

- Cross-exchange arbitrage involves buying an asset on one exchange where the price is lower and selling it immediately on another where the price is higher to profit from the difference. Price gaps are brief and require fast, cost-aware execution using APIs and pre-funded accounts to succeed. Market efficiency and trading fees often erode profits, making discipline in cost modeling and timing essential for traders.

Cross-exchange arbitrage is the simultaneous buying and selling of the same financial asset on different trading venues to profit from price disparities. In the industry, this practice is also called spatial arbitrage when geographic differences drive the price gap. The strategy targets temporary market inefficiencies, and price gaps often last seconds to minutes before markets self-correct. For traders and investors who understand the mechanics, these fleeting windows represent real, repeatable profit opportunities. The challenge is executing fast enough and cheaply enough to keep those profits intact.

What is cross-exchange arbitrage and why do price gaps exist?

Cross-exchange arbitrage works because markets update at different speeds and carry different levels of liquidity and friction. When Bitcoin trades at $67,200 on Coinbase and $67,450 on Binance at the same moment, a trader can buy on Coinbase and sell on Binance, pocketing the $250 difference before the gap closes. That gap exists because no single pricing authority governs all exchanges simultaneously.

Several conditions create these discrepancies:

- Liquidity differences. A thinly traded exchange reacts more slowly to global price moves, creating a lag versus a high-volume venue.

- Latency gaps. Order books on different platforms refresh at different speeds, leaving brief windows of misalignment.

- Geographic and regulatory factors. Regional demand and fiat currency fluctuations create persistent price differences across borders. The “kimchi premium,” where Korean crypto markets have historically priced Bitcoin higher than Western exchanges, is a well-documented example of geographic arbitrage opportunities.

- Local demand spikes. A news event in one region can drive buying on local exchanges before global platforms catch up.

The core insight is that price convergence is inevitable. Markets are self-correcting. Your job as an arbitrageur is to act before that correction happens.

Pro Tip: Track multiple exchanges for the same asset simultaneously. A single-exchange view hides the price gaps that make arbitrage possible.

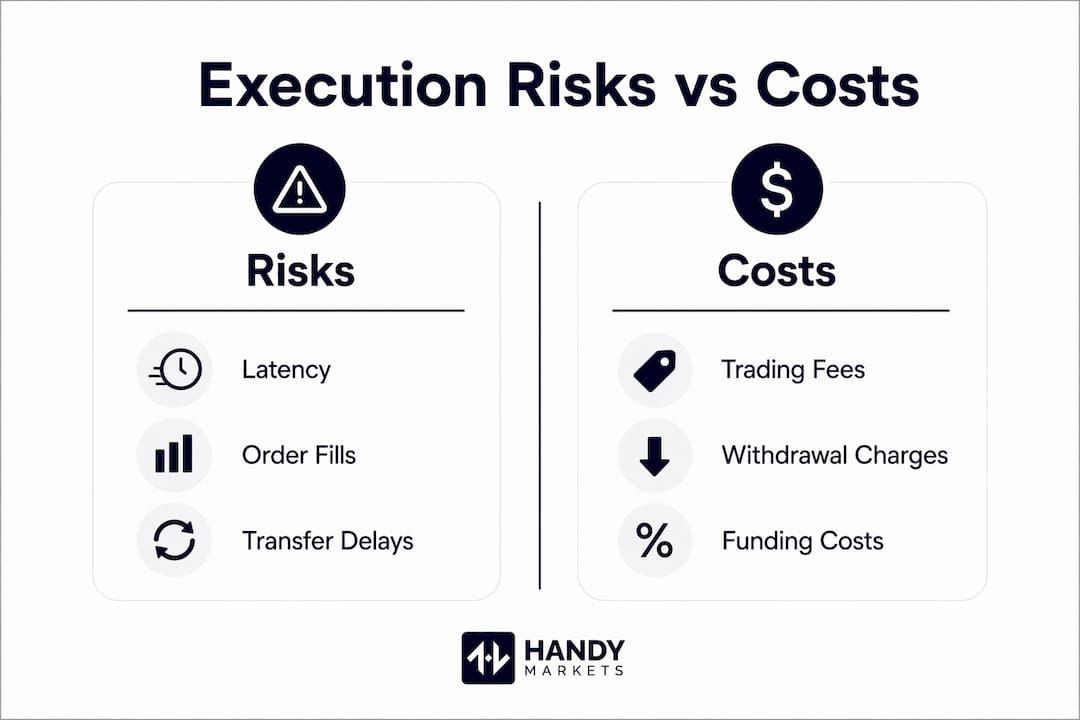

What execution risks and costs affect cross-exchange arbitrage profits?

Real cross-exchange arbitrage carries risks that raw price comparisons never show. A $200 price gap looks attractive until you subtract trading fees, withdrawal costs, and the slippage from executing a large order. What remains is often far less than expected, and sometimes negative.

The main execution risks include:

- Latency risk. By the time your order reaches the exchange, the price may have moved. High-frequency traders and bots compete for the same gaps.

- Partial fills. Your buy order may fill completely while your sell order fills only partially, leaving you exposed to price movement on the unfilled portion.

- Settlement and transfer delays. Moving assets between exchanges takes time. Blockchain confirmations for crypto can take minutes, during which the price gap may close or reverse.

- Funding risk. Holding capital on multiple exchanges simultaneously ties up liquidity and exposes you to exchange-specific risks like outages or insolvency.

The cost side is equally demanding. Calculating cost-aware spreads rather than raw price gaps is the difference between a profitable trade and a losing one. A cost-aware spread compares the actual executable buy price on one exchange against the actual executable sell price on another, after factoring in bid/ask spreads, trading commissions, withdrawal fees, and any financing costs. Many traders focus on raw price differences instead of tradable spreads after fees, which leads to false confidence in opportunities that do not actually exist.

Pro Tip: Before placing any arbitrage trade, build a simple cost model. List every fee on both sides of the trade. If the net spread after all costs is not clearly positive, skip the trade.

How to implement cross-exchange arbitrage strategies effectively

Successful implementation depends on speed, preparation, and the right tools. APIs and automated bots are the standard approach for serious arbitrageurs because manual execution is too slow for most opportunities. A bot can monitor price feeds across multiple exchanges, calculate cost-aware spreads in real time, and submit orders within milliseconds.

Here is a practical framework for getting started:

- Select your target assets and exchanges. Focus on assets with high trading volume and multiple active exchanges. Bitcoin, Ethereum, and major forex pairs offer the most frequent discrepancies. Compare exchanges by fee structure, API reliability, and withdrawal speed.

- Pre-fund accounts on multiple exchanges. Holding assets pre-funded on both sides eliminates transfer delays. If you plan to arbitrage Bitcoin between two exchanges, keep Bitcoin on the sell-side exchange and stablecoins or fiat on the buy-side exchange before the opportunity appears.

- Connect via API and monitor order book depth. Executable prices come from the order book, not the last trade price. A $200 gap at the top of the book may shrink to $50 when you account for the actual depth available at that price.

- Set price alerts for fast opportunity detection. Tools like Handy Markets let you configure real-time price alerts across Telegram, Discord, Slack, SMS, and email, so you catch significant price moves the moment they occur.

- Execute both legs as close to simultaneously as possible. True simultaneity is the goal. The longer the gap between your buy and sell execution, the more market risk you carry.

Choosing the right exchanges for arbitrage

| Factor | What to look for |

|---|---|

| Trading fees | Lower maker/taker fees preserve more of the spread |

| API speed | Faster API response times reduce latency risk |

| Withdrawal limits | High limits allow larger position sizes |

| Asset availability | Both exchanges must list the same asset |

| Liquidity depth | Deep order books reduce slippage on larger trades |

You can review market aggregator tools to compare live prices across exchanges in one place, which cuts the time needed to spot discrepancies manually.

How does cross-exchange arbitrage compare to other arbitrage types?

Cross-exchange arbitrage is one of several distinct strategies in the arbitrage family. Understanding the differences helps you choose the right approach for your capital, technology, and risk tolerance.

Triangular arbitrage exploits price differences within multiple currency or asset pairs on a single exchange. For example, a trader might cycle through Bitcoin, Ethereum, and USDT on one platform, profiting from a pricing inconsistency in the three pairs. Triangular arbitrage avoids cross-exchange transfer risks entirely but requires more complex calculations and faster execution logic.

Statistical arbitrage uses quantitative models to identify assets that historically move together and trade the divergence when they temporarily separate. It is less time-sensitive than cross-exchange arbitrage but requires significant modeling expertise and carries more directional risk.

| Arbitrage type | Execution venue | Key risk | Complexity |

|---|---|---|---|

| Cross-exchange | Multiple exchanges | Transfer delays, latency | Moderate |

| Triangular | Single exchange | Execution speed, model error | High |

| Statistical | Single or multiple | Model risk, directional exposure | Very high |

| Spatial (geographic) | Multiple regions | Regulatory barriers, FX risk | Moderate to high |

Cross-exchange arbitrage sits in a practical middle ground. It is more accessible than statistical arbitrage and more straightforward than triangular strategies, but it demands fast execution and careful cost management. For traders who want a clear, rules-based approach to exploiting market inefficiencies, cross-exchange arbitrage is often the best starting point. You can also review an arbitrage trading checklist to make sure your process covers every operational step before you go live.

Key takeaways

Cross-exchange arbitrage profits depend on cost-aware execution, pre-funded accounts, and speed, not just finding a raw price gap between two venues.

| Point | Details |

|---|---|

| Price gaps are temporary | Discrepancies last seconds to minutes, so fast execution is non-negotiable. |

| Costs erode raw spreads | Always calculate fees, spreads, and withdrawal costs before entering a trade. |

| Pre-funding saves time | Holding assets on both exchanges eliminates transfer delays that kill opportunities. |

| Technology is required | APIs and automated bots are the standard tools for competitive arbitrage execution. |

| Know your arbitrage type | Cross-exchange arbitrage is more accessible than triangular or statistical strategies. |

The reality of arbitrage that most traders learn too late

We have watched traders enter cross-exchange arbitrage with genuine excitement, only to find their first few trades barely break even. The reason is almost always the same: they measured the opportunity by the raw price gap and ignored the full cost stack. A $300 spread sounds like free money until you subtract a 0.1% maker fee on each side, a $15 withdrawal fee, and 0.05% slippage on a $50,000 position. Suddenly that trade costs more than it earns.

The other hard lesson is speed. Markets in 2026 are more efficient than they were five years ago. Retail traders competing manually against institutional bots running co-located servers are at a structural disadvantage on the fastest opportunities. That does not mean arbitrage is closed to individual traders. It means you need to be selective. The opportunities worth chasing are the ones where your cost structure gives you an edge, not just the ones where a price gap exists.

What we find most encouraging is that disciplined traders who build proper cost models, pre-fund accounts, and use alert tools consistently find tradable opportunities. The market is large enough. The key is patience and process over impulse.

How Handy Markets supports your arbitrage monitoring

Spotting a price discrepancy before it closes requires real-time data across multiple markets at once. Handy Markets aggregates live prices across cryptocurrencies, stocks, forex, commodities, and indices in one place, giving you the cross-market visibility that arbitrage demands.

Price alerts on Handy Markets deliver notifications through Telegram, Discord, Slack, SMS, Webhook, and Email the moment an asset hits your target price. That speed matters when opportunities last only seconds. You can track live market prices across asset classes and configure alerts for the specific pairs you are watching, so you are always positioned to act when a gap appears. Setup takes minutes, and the core alert features are free.

FAQ

What is cross-exchange arbitrage in simple terms?

Cross-exchange arbitrage is buying an asset on one exchange where the price is lower and simultaneously selling it on another exchange where the price is higher. The profit comes from the price difference, minus all fees and costs.

How long do cross-exchange arbitrage opportunities last?

Price gaps between exchanges typically last seconds to minutes before markets self-correct. Automated bots and APIs are the standard tools for capturing these short windows.

What are the biggest risks in cross-exchange arbitrage?

The main risks are latency, partial order fills, transfer delays, and trading fees that erode the spread. Operational failures like exchange outages can also turn a planned profit into a loss.

Is cross-exchange arbitrage legal?

Cross-exchange arbitrage is legal in most jurisdictions. It is a standard trading strategy that improves market efficiency by reducing price discrepancies across venues.

How is cross-exchange arbitrage different from triangular arbitrage?

Cross-exchange arbitrage trades the same asset across different exchanges. Triangular arbitrage exploits pricing inconsistencies between multiple trading pairs on a single exchange, avoiding transfer risks but requiring more complex execution logic.