TL;DR:

- Forex introduces currency risk into portfolios, often increasing volatility without reliable returns if unmanaged. Strategic hedging and deliberate exposure can reduce risks and enhance risk-adjusted returns across asset classes. Active monitoring and disciplined rebalancing are essential for effective currency position management.

Forex, formally known as the foreign exchange market, is defined as the mechanism through which currency risk enters every internationally diversified portfolio, whether investors intend it or not. The role of forex in portfolios extends far beyond speculative trading. It functions as both a source of uncompensated volatility and a deliberate diversification tool that, when managed with precision, can improve risk-adjusted returns across equities, bonds, and alternative assets. Portfolio managers who treat currency exposure as strategic, rather than accidental, consistently achieve better outcomes than those who ignore it. This guide explains exactly how to do that.

How does the role of forex in portfolios affect volatility and returns?

Currency risk is the single most underestimated source of volatility in globally diversified portfolios. When you hold international equities or bonds, you automatically inherit the exchange rate movements between your home currency and the asset’s denomination. That exposure is not neutral.

Currency risk adds 3 to 5% of annualized volatility to unhedged portfolios without delivering a reliable return premium in exchange. That means you are absorbing real risk with no structural compensation, which is the definition of an inefficient exposure. For a portfolio targeting 10% annualized volatility, an unhedged currency layer can represent 30 to 50% of total risk budget, consumed by an exposure that was never consciously chosen.

The impact is not uniform across asset classes:

- International equities carry moderate currency risk. Because equity returns are volatile themselves, the currency layer represents a smaller proportional share of total risk. Selective exposure can even reduce overall portfolio volatility in some cases.

- International bonds are far more sensitive. Bond returns are lower and more stable, so currency swings can easily dwarf the underlying yield. An unhedged foreign bond position often behaves more like a currency bet than a fixed-income allocation.

- Emerging market assets compound the problem. Currency volatility in developing economies can exceed 15% annualized, dwarfing the asset’s fundamental return.

A study of Australian dollar portfolios found that FX exposure reduced equity volatility by 3.7% per annum, illustrating that selective currency exposure, when chosen deliberately, can actually dampen total portfolio risk rather than amplify it. The key word is deliberately. Passive exposure without a framework is where portfolios get hurt. You can read more about the mechanics of forex volatility drivers to understand what moves exchange rates at the macro level.

What are optimal forex hedging strategies in portfolios?

Hedging is the primary tool for managing the impact of forex on investments, and the optimal approach depends heavily on which asset class you are protecting. The research is clear on this point.

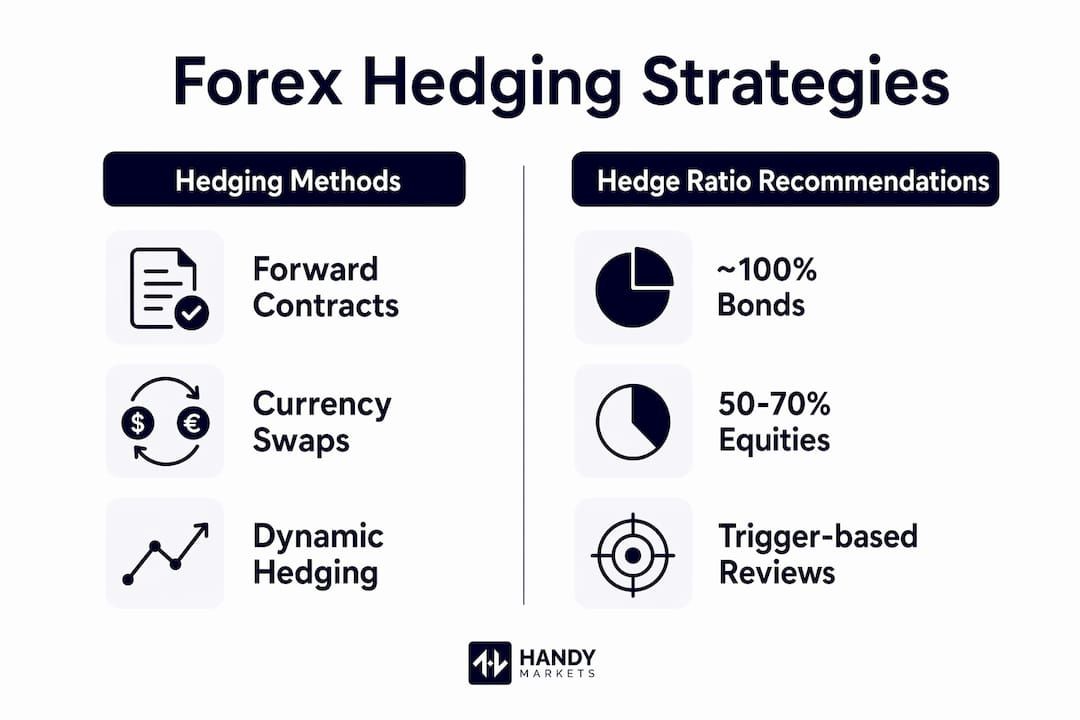

Optimal hedge ratios sit near 100% for international bonds and between 50 and 70% for developed market equities. For bonds, full hedging is almost always justified because currency volatility overwhelms fixed-income returns. For equities, partial hedging preserves some diversification benefit while controlling excess volatility.

The table below summarizes how hedging approaches differ by asset class and investor objective:

| Asset class | Recommended hedge ratio | Primary rationale |

|---|---|---|

| International bonds | ~100% | Currency volatility exceeds yield; full hedge preserves return profile |

| Developed market equities | 50 to 70% | Partial hedge balances diversification with volatility control |

| Emerging market equities | Case by case | Hedging costs often high; selective exposure may be preferable |

| Commodities (USD-priced) | Depends on home currency | USD-denominated assets create implicit USD exposure |

Partial currency hedging balances FX diversification and volatility reduction in international equities, which is why most institutional managers do not hedge to 100% across their equity book. Removing all currency exposure from equities eliminates a genuine diversification benefit, particularly when your home currency and the foreign currency have low or negative correlation.

The two primary hedging instruments are forward contracts and currency swaps. Forwards lock in an exchange rate for a future date and are the most common tool for portfolio hedging. Swaps are used for longer-duration exposures or when cash flow management matters. Both carry a cost, typically the interest rate differential between the two currencies, which can be positive or negative depending on the rate environment.

Dynamic hedging adjusts the hedge ratio over time based on market conditions, currency valuations, or volatility signals. Static hedging sets a fixed ratio and rebalances periodically. Dynamic approaches can add value but require active monitoring and generate higher transaction costs. For most portfolio managers, a semi-static approach, reviewing hedge ratios quarterly and adjusting when exposures drift significantly, strikes the right balance. You can explore hedging strategies in forex in more depth to understand the mechanics of forwards and swaps in practice.

Pro Tip: Set a hedge ratio review trigger, not just a calendar schedule. If your currency exposure drifts more than 10 percentage points from your target due to market moves, rebalance immediately rather than waiting for the next quarterly review.

How can forex diversification strategies enhance portfolios beyond hedging?

Hedging manages risk. Active forex strategies can generate returns. The distinction matters because the two objectives require different frameworks and different risk tolerances.

The most widely used active forex strategy is the carry trade, which involves borrowing in a low-interest-rate currency and investing in a higher-yielding one to earn the interest rate differential. Carry trades earn the interest differential between two currencies, and over long horizons, this strategy has delivered positive expected returns across multiple market cycles.

Here is how a carry trade works in practice:

- Identify the spread. Find two currencies with a meaningful interest rate differential. Historically, the Japanese yen (JPY) as a funding currency against the Australian dollar (AUD) or New Zealand dollar (NZD) has been a classic example.

- Size the position. Allocate capital proportional to your risk budget, not the yield. The carry looks attractive until it unwinds.

- Monitor macro triggers. Risk-off events, central bank pivots, and geopolitical shocks are the primary catalysts for carry unwinds.

- Set exit criteria. Define the volatility level or drawdown threshold at which you reduce or close the position before losses compound.

The critical risk is the unwind. Carry trades pay steady returns but can lose large amounts in occasional crashes. The 2008 financial crisis and the August 2024 JPY carry unwind are textbook examples of how quickly these positions can reverse. Position sizing must account for possible large unwinds, not just expected carry. This is the mistake most retail participants make.

“True forex diversification requires holdings of currency pairs with distinct macro drivers to avoid hidden correlations and concentration risks.” — Vantage Markets

Beyond carry, safe-haven currencies serve a different portfolio function. The USD, JPY, and CHF tend to appreciate during equity sell-offs, acting as shock absorbers when risk assets fall. Holding deliberate exposure to these currencies can reduce portfolio drawdowns during stress periods. The caveat is that correlation patterns are unstable during systemic crises, so safe-haven properties cannot be relied upon unconditionally.

A common pitfall in forex trading within portfolios is false diversification. Holding EUR/USD, GBP/USD, and AUD/USD together increases hidden USD correlation and concentration risk. All three pairs move partly in response to USD dynamics, so the apparent diversification across three positions is illusory. True diversification requires pairs with genuinely distinct macro drivers, such as combining a commodity currency (AUD), a safe-haven currency (CHF), and an emerging market currency with independent policy cycles. Explore diversified portfolio construction for a deeper look at how professionals structure multi-currency allocations.

How to implement forex exposure effectively within an investment portfolio

Knowing the theory is one thing. Translating it into a functioning portfolio process is where most managers either succeed or stumble. Here is a practical framework for integrating forex exposure without letting it dominate your risk budget.

Start with a currency audit. Before adding any active forex positions, map every existing currency exposure in your portfolio. International equities, foreign bonds, commodity holdings priced in USD, and even cash held in foreign accounts all carry implicit currency risk. Most portfolios have far more forex exposure than their managers realize.

Set explicit currency allocation targets. Treat currency exposure the same way you treat equity or fixed-income allocation. Define target weights, acceptable ranges, and rebalancing triggers for each major currency. This converts accidental exposure into a deliberate allocation.

Key risk management practices for forex trading in portfolios include:

- Position sizing based on volatility, not notional value. A 1% allocation to a high-volatility emerging market currency pair carries far more risk than a 5% allocation to a stable G10 pair.

- Stop-loss levels tied to portfolio impact, not pip counts. Define the maximum acceptable drawdown contribution from any single currency position before entering the trade.

- Correlation monitoring across the full portfolio. Currency positions interact with equity and bond holdings in ways that are not always obvious. A long USD position may hedge your international equity book but amplify losses if your domestic equity holdings also fall during a USD rally.

- Cost accounting for hedging instruments. Forward contracts and swaps carry implicit costs through the interest rate differential. In a high-rate environment, hedging USD exposure from a lower-rate home currency can cost 3 to 5% annually, which must be weighed against the volatility reduction benefit.

Pro Tip: Use live exchange rate data to monitor currency correlations in real time. Correlations shift with macro regimes, and a hedge that worked in 2024 may not perform the same way in 2026’s rate environment.

Monitoring tools matter here. Platforms that aggregate live forex and market data allow portfolio managers to track currency movements alongside equity and bond positions, giving a unified view of total portfolio risk rather than managing each asset class in isolation.

Key takeaways

Forex functions as both a risk factor and a diversification tool in portfolios, and the outcome depends entirely on whether the exposure is managed with intention or left to chance.

| Point | Details |

|---|---|

| Currency risk is uncompensated | Unhedged FX adds 3 to 5% annual volatility without a reliable return premium. |

| Hedge ratios vary by asset class | Use near 100% for bonds and 50 to 70% for developed market equities. |

| Carry trades require unwind discipline | Size carry positions for crash scenarios, not just expected yield. |

| False diversification is a real trap | Multiple USD-correlated pairs create concentration risk, not true diversification. |

| Active monitoring changes outcomes | Treating currency exposure as a deliberate allocation improves risk-adjusted returns. |

The forex mistake most portfolios are still making

At Handy, we track currency data across dozens of markets daily, and one pattern stands out consistently. Most investors acknowledge currency risk in theory but manage it reactively in practice. They hedge after volatility spikes, not before. They add carry trades when yields look attractive without stress-testing the unwind scenario. And they hold three or four currency pairs that all respond to the same USD driver, believing they have diversified when they have only multiplied their exposure.

The 2026 rate environment makes this more consequential than it was two years ago. Central bank divergence between the Federal Reserve, the European Central Bank, and the Bank of Japan has widened interest rate differentials significantly, making carry trades more tempting and more dangerous simultaneously. The JPY carry unwind of August 2024 was a preview of what happens when a crowded trade reverses in a risk-off environment.

Our view is that the most resilient portfolios treat currency allocation the same way they treat equity sector weights. They set targets, monitor drift, and rebalance with discipline. The managers who do this do not eliminate currency risk. They convert it from a passive liability into a managed position with a defined role in the portfolio. That shift in mindset is worth more than any specific hedging ratio or carry strategy.

Monitor your forex exposure with Handy.Markets

Managing the role of forex in your portfolio starts with having the right data at the right time. Handy.Markets gives you live exchange rates, percentage changes, and price movement alerts across all major and emerging market currency pairs, alongside your equity, bond, and commodity holdings in one place.

Set up custom forex price alerts via Telegram, Discord, Slack, SMS, or email so you never miss a critical currency move that could affect your portfolio’s risk profile. Whether you are monitoring a carry trade position or tracking a hedging trigger, Handy delivers the signal before the market moves past your threshold. Explore the full markets dashboard to see live forex data alongside every other asset class in your portfolio, all in one view.

FAQ

What is the role of forex in investment portfolios?

Forex serves as both a source of currency risk and a diversification tool in investment portfolios. When managed strategically, it can improve risk-adjusted returns by reducing volatility through hedging or adding incremental returns through carry and safe-haven strategies.

How does currency risk affect portfolio volatility?

Unhedged currency exposure adds 3 to 5% of annualized volatility to a portfolio without delivering a reliable return premium. For bond-heavy portfolios, this effect is especially pronounced because currency swings can exceed the underlying yield.

What hedge ratio should I use for international equities?

Research supports hedge ratios of 50 to 70% for developed market equities, which balances volatility reduction with the preservation of diversification benefits. International bonds warrant near-full hedging because their lower return profile makes them far more sensitive to currency swings.

Are carry trades a reliable forex investment strategy?

Carry trades offer positive expected returns over long horizons but are vulnerable to sharp, crisis-driven unwinds that can erase months of gains in days. Position sizing must account for unwind risk, not just the expected interest differential.

How do I avoid false diversification in forex trading?

True forex diversification requires currency pairs with distinct macro drivers. Holding EUR/USD, GBP/USD, and AUD/USD together creates hidden USD concentration risk rather than genuine diversification. Combine pairs from different economic regions with independent policy cycles to reduce correlation.