TL;DR:

- Understanding the full range of asset classes, from cash to cryptocurrencies, helps investors manage risk and seize opportunities more effectively. Asset classes are broad groups sharing similar risk and return characteristics, with traditional four being cash, bonds, equities, and real assets, while alternatives include commodities, private equity, hedge funds, and crypto. Since classifications depend on context and sub-classes, continuous learning and regime-aware adjustments are essential for building resilient portfolios that adapt to macroeconomic shifts.

Most investors think asset classes are just stocks and bonds. That view leaves a lot of money, risk, and opportunity completely off the table. Understanding asset classes in their full breadth, from cash and real estate to private equity and cryptocurrency, is what separates a reactive investor from a confident one. This guide cuts through the noise to give you a working framework for every major investment category, how they behave, why they matter, and how to use that knowledge to build a portfolio that actually reflects your goals.

Table of Contents

- Key takeaways

- Understanding asset classes: the traditional four

- Alternative and emerging asset classes

- How to classify assets: nuances and overlaps

- Asset classes and portfolio diversification

- How macro conditions reshape asset class behavior

- My perspective on getting asset class investing right

- Track every asset class with Handy

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Asset classes group similar investments | Each class shares risk/return characteristics, helping you analyze and manage your portfolio systematically. |

| Traditional and alternative classes differ | Cash, bonds, equities, and real estate form the core. Commodities, crypto, and private equity add complexity and opportunity. |

| No universal classification exists | How assets get categorized depends on context, investor type, and regulatory framework. |

| Diversification reduces single-source risk | Mixing asset classes protects your portfolio when one category underperforms. |

| Macro conditions change class behavior | Inflation, interest rates, and market regimes shift how each class performs, requiring ongoing attention. |

Understanding asset classes: the traditional four

The phrase “asset class” gets used constantly in finance, yet asset classes are simply broad groupings of investments that share similar economic characteristics and sources of risk and return. Think of each class as a family with its own personality. Knowing that personality helps you predict how it will behave under pressure.

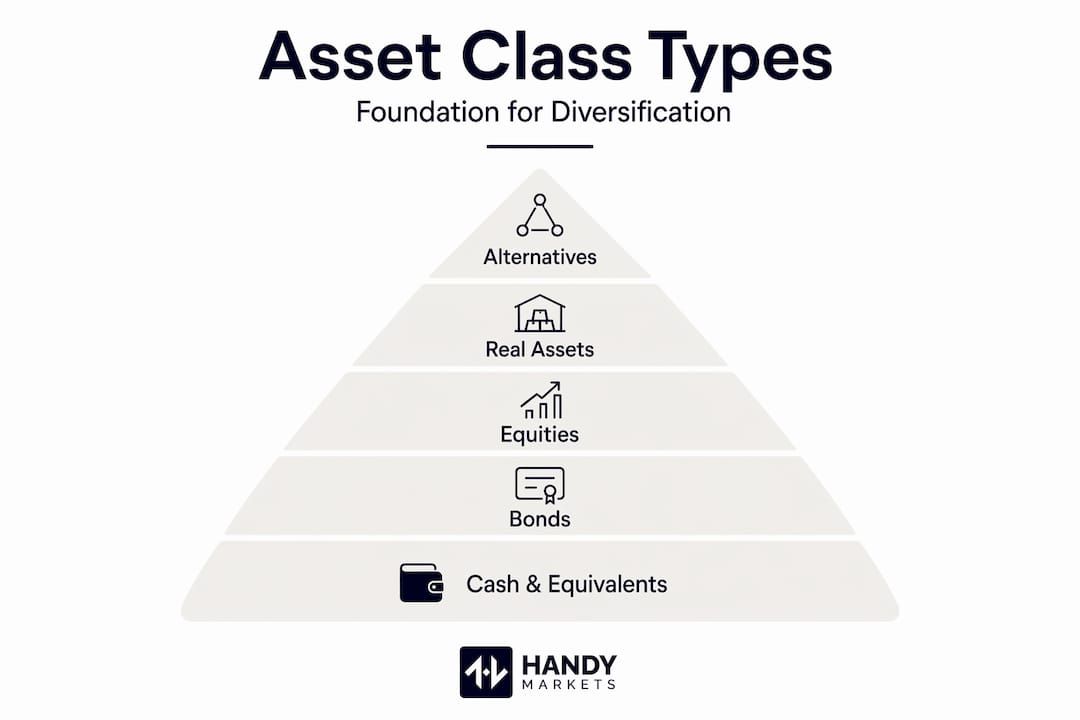

The four traditional classes every investor should know are cash, fixed income, equities, and real assets.

- Cash and cash equivalents include savings accounts, money market funds, and Treasury bills. These are the most liquid assets you can hold. They carry almost no credit risk, but they also offer minimal growth. Their primary job is to give your portfolio a stable floor and keep funds accessible for short-term needs or opportunistic buying.

- Fixed income (bonds) represents debt securities issued by governments and corporations. You lend money, and in return you receive regular interest payments plus your principal back at maturity. Bonds generally sit between cash and stocks on the risk spectrum. A useful practical tool here is the bond ladder, which staggers maturities for reinvestment, reducing your sensitivity to interest rate swings over time.

- Equities (stocks) represent ownership stakes in companies. They carry the highest volatility of the traditional four but also the strongest long-term growth potential. Within equities, two investors can own stocks in the same broad class and still face very different risk profiles depending on factors like company size, sector, and geography.

- Real assets cover real estate, infrastructure, and land. They tend to act as an inflation hedge because their value often rises alongside prices for goods and services. Real estate investment trusts (REITs) let everyday investors access this class without buying physical property.

The table below gives you a fast comparison to anchor these distinctions.

| Asset class | Typical return potential | Volatility | Liquidity | Primary portfolio role |

|---|---|---|---|---|

| Cash equivalents | Very low | Minimal | Very high | Stability and accessibility |

| Fixed income | Low to moderate | Low to moderate | Moderate to high | Income and risk buffer |

| Equities | High | High | High | Long-term growth |

| Real assets | Moderate to high | Moderate | Low to moderate | Inflation protection |

Pro Tip: Do not judge a bond or stock purely by its class label. As individual investment behavior shows, two assets in the same class can carry very different credit risk, quality, and return potential depending on sub-class and geography.

Alternative and emerging asset classes

If the traditional four are the foundation, alternative asset classes are the floors you add on top. They are not for everyone, but ignoring them entirely means missing legitimate diversification tools.

What makes an asset “alternative”? Broadly, alternative classes are those that fall outside conventional stocks, bonds, and cash. They typically come with lower liquidity, higher complexity, and less regulatory transparency. But they also carry distinct return characteristics that may not move in sync with your traditional holdings, which is precisely why many institutional investors use them.

Here are the key categories:

- Commodities include gold, oil, agricultural products, and industrial metals. They respond directly to supply-demand dynamics and inflation. Gold, in particular, is historically sought during market stress as a store of value.

- Private equity involves direct investment in companies that are not publicly traded. Returns can be significant, but your capital is typically locked up for years. This is generally suitable for accredited investors with long time horizons.

- Hedge funds use pooled capital and flexible strategies, including short-selling, leverage, and derivatives, to seek returns regardless of market direction. They are complex, fee-heavy, and typically accessible only to institutional or high-net-worth investors.

- Cryptocurrencies are the newest recognized category. Assets like Bitcoin and Ethereum operate on decentralized networks and are not correlated with traditional markets in the same predictable way. They offer high return potential alongside extreme volatility and evolving regulatory risk.

Pro Tip: Before adding any alternative asset, honestly assess your liquidity needs. Private equity and hedge funds may lock up capital for three to ten years. Crypto is liquid but can swing 30% or more in a single week. Know what you are signing up for before committing.

Understanding these categories connects to the broader topic of financial assets, including how different standards and regulators define their boundaries.

How to classify assets: nuances and overlaps

Here is a truth that many beginner guides skip over. There is no universal classification system for asset classes. Whether something counts as its own class, a sub-class, or an investment strategy depends entirely on who is doing the classifying: a regulator, an accountant, an institutional investor, or a retail platform.

That matters because the label alone does not tell you everything you need to know. Here are the key criteria professionals use when classifying assets:

- Homogeneity of risk and return. Assets in the same class should respond similarly to the same economic forces. If two investments react very differently to rising interest rates, they likely belong in different categories.

- Shared systematic risk factors. Inflation, interest rates, credit spreads, and liquidity conditions all drive correlations across classes, especially during market stress when diversification benefits tend to shrink rather than grow.

- Regulatory and accounting context. Pension funds, insurance companies, and retail brokerages may categorize the same instrument differently depending on the rules that govern them.

- Sub-class distinctions. REITs are technically equities but behave more like real assets. High-yield bonds share a class label with investment-grade bonds but carry credit risk closer to equities. The sub-class often matters more than the parent class.

Pro Tip: When building a portfolio, go one level deeper than the class label. Knowing you own “bonds” is less useful than knowing whether those bonds are short-duration Treasuries or long-duration corporate debt. Each behaves very differently when rates change.

Asset classes and portfolio diversification

The whole point of learning how to classify assets is to apply that knowledge. And the most direct application is building a portfolio that does not rely on a single engine for performance.

Different asset classes respond differently to economic growth, inflation, and market stress. Equities tend to flourish when the economy grows. Bonds typically rise when growth slows and rates fall. Real assets protect when inflation accelerates. Cash sits quietly as a reserve. When you mix these classes deliberately, you reduce the chance that one bad environment destroys your whole portfolio.

Consider a simplified allocation model used as a reference point by many advisors.

| Investor profile | Equities | Fixed income | Real assets | Cash/alternatives |

|---|---|---|---|---|

| Aggressive growth | 80% | 10% | 7% | 3% |

| Balanced | 60% | 25% | 10% | 5% |

| Conservative income | 30% | 50% | 10% | 10% |

These are starting points, not prescriptions. The key principles behind diversification include:

- Correlation matters more than count. Owning ten assets that all fall together in a recession is not diversification. You want assets that respond to different drivers.

- Rebalancing is the mechanism. Allocations drift as asset prices move. Rebalancing back to your targets periodically sells what has risen and buys what has fallen, which is a disciplined way to buy low.

- Beware false diversification. Many investors think they are diversified because they own many stocks across sectors. But diversification across asset classes is fundamentally different from diversification within a single class.

For readers who also want to explore diversifying a portfolio specifically in foreign exchange markets, the principles of correlation-aware allocation apply there as well.

How macro conditions reshape asset class behavior

Even a well-constructed portfolio needs recalibration over time. Markets do not stay in one regime forever, and the relationships between asset classes shift as macroeconomic conditions evolve.

Research into distinct financial market eras shows that factors like technology competition, geopolitical tension, and inflation regimes affect the equity risk premium and bond returns in ways that long-run historical averages simply cannot capture. Specifically, a technology-war era tends to increase the equity risk premium while compressing bond returns, which alters the typical 60/40 portfolio logic.

“Investors should calibrate asset allocation to current financial regimes rather than historical averages, as expected returns and risk dynamics shift by era.” CFA Institute Research Foundation

Practically, this means watching three macro variables closely. First, inflation. Rising inflation tends to erode fixed income returns while lifting real assets and commodities. Second, interest rates. Higher rates compress bond prices and can slow equity valuations. Third, credit conditions. When credit spreads widen, it signals stress, and correlations between classes tend to rise, reducing your diversification benefit right when you need it most.

Pro Tip: Rather than shifting your entire allocation every time conditions change, consider a core and satellite approach. Keep a stable core allocation and use smaller satellite positions in macro-sensitive assets like commodities or short-duration bonds to express your current regime view without overturning your long-term plan.

My perspective on getting asset class investing right

I have seen a lot of investors approach their portfolios with a mental model that is years out of date. The standard advice about stocks and bonds being enough to diversify has held up in some eras and badly underperformed in others, and the difference almost always comes down to whether someone understood the sub-classes they actually owned and the macro environment they were operating in.

What I have found working with market data across multiple asset classes is that the label is the beginning of understanding, not the end. Knowing you own “equities” tells you far less than understanding whether those are large-cap growth stocks in a rate-rising environment or small-cap value names in an inflationary cycle. The nuances drive the outcomes.

My honest advice is to resist the pull of rigid allocation formulas. The investment strategies that hold up across cycles share one quality: they are built around awareness, not habit. Stay curious. Study how each class behaves under the conditions currently in play, not just how they behaved historically.

Track every asset class with Handy.Markets

Once you understand the theory, you need the tools to act on it. Handy makes it practical.

Handy.markets aggregates live prices and percentage changes across stocks, bonds, commodities, cryptocurrencies, indices, and forex, so you can see your entire investment universe in one place. No more toggling between tabs or missing a move while you are offline. You can set price alerts delivered through Telegram, Discord, Slack, SMS, Email, or Webhook, so critical market movements reach you instantly through the channel you actually check. If cryptocurrency is part of your allocation, you can track assets like Assisterr AI (ASRR) with instant notifications the moment a target price is hit. You can also explore ETFs across asset classes to compare live prices and set alerts on funds that span multiple investment categories. Handy turns asset class knowledge into real-time awareness.

FAQ

What are asset classes in simple terms?

An asset class is a group of investments that share similar economic characteristics and respond to the same risk factors. Core examples include stocks, bonds, real estate, and cash.

Why does understanding asset classes matter for investors?

Knowing how different asset classes behave under various economic conditions allows you to build a portfolio that spreads risk intelligently, so a drop in one category does not wipe out your entire position.

How many asset classes are there?

There is no fixed number because no universal classification system exists. Most frameworks recognize four to six traditional classes, with alternatives like private equity, hedge funds, commodities, and cryptocurrencies adding further categories depending on context.

Can two investments in the same asset class behave differently?

Yes, significantly. Within any class, factors like credit quality, sub-class, geographic exposure, and duration mean that two bonds or two stocks can carry very different risk and return profiles.

How often should I review my asset class allocation?

Most advisors recommend reviewing allocations at least annually, and also after major market regime shifts, such as a significant change in interest rates or inflation, which can alter how each class contributes to your portfolio.