TL;DR:

- Diversification lowers risk by combining assets that do not move in lockstep, without sacrificing returns. Proper implementation requires understanding correlations, avoiding overconcentration, and regularly rebalancing to maintain resilience against market shifts. True diversification involves spanning asset classes, geographies, and strategies to optimize risk-adjusted performance.

Most investors believe that spreading money across more assets automatically waters down their returns. That belief is wrong, and it’s costing portfolios real money. Harry Markowitz’s Modern Portfolio Theory (1952) formalized this as mean-variance optimization, famously calling diversification “the only free lunch in finance.” The core insight is striking: you can lower risk without proportionally sacrificing return, simply by owning assets that don’t move in lockstep. This article breaks down the theory, the math, and the practical steps you need to build a genuinely resilient portfolio.

Table of Contents

- The foundations of portfolio diversification

- How diversification actually reduces risk

- Types of diversification: Not just stocks vs. bonds

- Practical steps to diversify your portfolio

- Why most investors get diversification wrong (and how to do better)

- Track, diversify, and manage your investments with Handy.Markets

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Diversification reduces risk | Combining assets with low correlation can significantly smooth returns and lower portfolio volatility. |

| Cross-asset portfolios perform better | Mixing stocks, commodities, and bonds outperforms single-asset portfolios, especially after 2009. |

| Correlation matters most | True diversification relies on how assets move relative to each other, not just owning many investments. |

| Review and rebalance | Regularly check and adjust your portfolio to stay diversified and aligned with your goals. |

The foundations of portfolio diversification

Portfolio diversification means spreading your investments across different assets, sectors, or geographies so that a loss in one area doesn’t wipe out your entire portfolio. Think of it like routing water through multiple pipes instead of one. If one pipe clogs, the flow continues. Your capital works the same way.

“Diversification is the only free lunch in finance.” — Harry Markowitz, 1952

Markowitz’s Modern Portfolio Theory showed mathematically that an investor can construct a portfolio that delivers the highest possible expected return for a given level of risk. This is called the efficient frontier, and it only exists because assets behave differently from each other under the same market conditions. When technology stocks fall sharply, government bonds often hold steady or rise. When emerging market equities surge, domestic large-caps may lag. That difference is what makes the math work in your favor.

Here’s what well-executed diversification actually delivers:

- Stabilized returns over time, reducing the emotional whiplash of sharp swings

- Lower overall portfolio volatility without eliminating all growth potential

- Reduced drawdown risk, meaning you lose less during market downturns

- Smoother compounding, because avoiding large losses lets you keep more capital working

Pro Tip: Diversification isn’t a set-it-and-forget-it move. The correlations between assets shift over time, especially during market stress, so your portfolio needs periodic attention to stay truly diversified.

The foundational principle is deceptively simple: own assets that react differently to the same economic events. But implementing it well requires understanding exactly how risk reduction works mathematically, which is where most investors stumble.

How diversification actually reduces risk

Understanding the concept is one thing. Here’s how diversification lowers risk in practice, and the numbers are genuinely surprising.

Imagine you hold two assets, each with 15% annual volatility (a standard measure of price swings). If those two assets are perfectly correlated, meaning they always move together, your portfolio volatility stays at 15%. No benefit. But if the two assets are uncorrelated, meaning their price movements are independent, your combined portfolio volatility drops to roughly 10%. You’ve cut risk by one-third without touching your expected returns. That’s the math Markowitz proved, and it holds up in real portfolios.

The key variable here is correlation, a number ranging from negative 1 to positive 1. Assets with a correlation of positive 1 move perfectly together. Assets at zero have no relationship. Assets at negative 1 move in exactly opposite directions. The lower the correlation between your holdings, the more effective your diversification becomes.

Here’s a simple reference table showing how correlation affects portfolio volatility when two assets each carry 15% volatility:

| Correlation between assets | Combined portfolio volatility |

|---|---|

| +1.0 (perfect positive) | 15.0% |

| +0.5 (moderate positive) | 12.4% |

| 0.0 (uncorrelated) | 10.6% |

| -0.5 (moderate negative) | 8.7% |

| -1.0 (perfect negative) | 0.0% |

The practical steps for applying this in your portfolio:

- Identify the volatility of each asset you currently hold, using standard deviation as your benchmark

- Estimate correlations between your holdings, which you can observe by comparing how assets perform during the same market events

- Add assets with low or negative correlations to your existing mix, such as commodities or Treasury bonds alongside equities

- Re-measure portfolio-level volatility after adding each new asset to confirm you’re actually reducing risk

Reviewing your volatility management strategy regularly matters because correlations are not static. During the 2020 COVID crash, for example, many assets that appeared uncorrelated suddenly moved together as panic selling hit every market at once. Similarly, Forex volatility can spike unpredictably based on interest rate decisions or geopolitical shifts, which ripples into equity and bond correlations.

Pro Tip: During extreme market stress, correlations between most risk assets tend to spike toward positive 1. This is why holding true diversifiers like gold or government bonds matters so much. They tend to hold their value or rise precisely when stocks are falling hardest.

One critical point: diversification does not guarantee profits, and it does not eliminate all risk. What it does is reduce the probability and magnitude of catastrophic losses, which gives your portfolio the resilience to recover and grow over time.

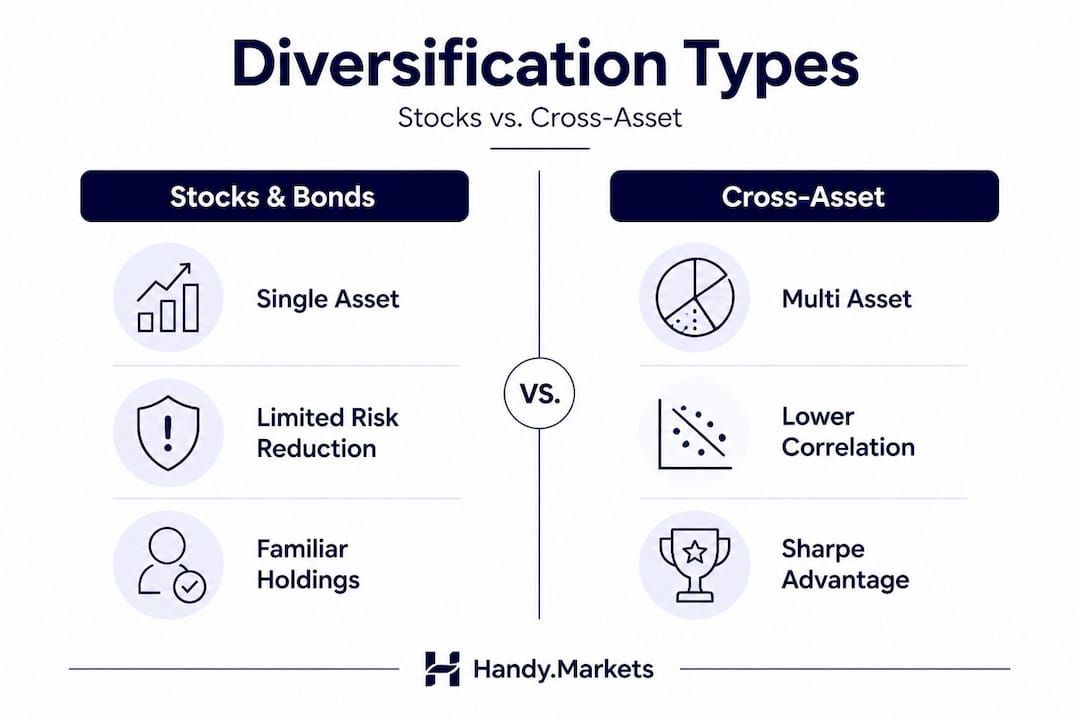

Types of diversification: Not just stocks vs. bonds

Now, let’s look at what real-world diversification means across the investment landscape. Most people think “diversified” means owning some stocks and some bonds. That’s a starting point, but it leaves a lot of risk-reduction potential on the table.

True diversification spans multiple dimensions:

- Asset class diversification: Stocks, bonds, commodities (gold, oil), real estate investment trusts (REITs), and cash equivalents. Each responds differently to inflation, interest rates, and economic cycles.

- Geographic diversification: U.S. equities, developed international markets (Europe, Japan), and emerging markets (India, Brazil). Economic growth cycles don’t align perfectly across regions.

- Sector diversification: Technology, healthcare, energy, consumer staples, financials. During the 2022 rate hike cycle, technology stocks fell 30%+ while energy stocks surged more than 50%.

- Alternative assets: Cryptocurrencies, private equity, hedge fund strategies, infrastructure. These often carry unique risk profiles that have low correlation with traditional assets.

The evidence for going beyond stocks and bonds is strong. Cross-asset diversification combining the S&P 500, gold, oil, and Treasury notes has outperformed U.S.-only or international stock portfolios since 2009, delivering higher Sharpe ratios (a measure of return per unit of risk).

Here’s a direct comparison of portfolio approaches:

| Portfolio type | Assets included | Approximate Sharpe ratio advantage | Key risk |

|---|---|---|---|

| U.S. stocks only | S&P 500 | Baseline | Concentration in one market |

| International stocks | Global equity index | Modest improvement | Currency risk, correlation creep |

| Cross-asset diversified | S&P 500 + gold + oil + T-notes | Significantly higher | Complexity, rebalancing discipline |

| Stocks + bonds + alternatives | Equities + fixed income + REITs + crypto | High (with careful selection) | Liquidity and volatility variation |

Exploring investment strategy comparisons can help you decide which mix fits your goals and risk tolerance. For investors who want exposure to multiple asset classes without building complex portfolios manually, ETF diversification offers a practical entry point with built-in variety and low costs.

One common pitfall is home bias, where investors overweight their domestic market because it feels familiar. U.S. investors, for example, often hold 80% or more of their equity allocation in U.S. stocks, even though the U.S. represents roughly 60% of global market capitalization. That overconcentration leaves returns tied too closely to the fortunes of a single economy.

Practical steps to diversify your portfolio

With the why and what covered, here’s how to put smart diversification into action. This isn’t abstract theory. These are concrete steps you can apply to your current portfolio this week.

- Audit your current holdings: List every position, note the asset class, sector, and geography. Many investors discover they’re far more concentrated than they realized, particularly in technology or domestic equities.

- Calculate or estimate correlations: Compare how your holdings performed during recent market events. Did everything fall together in 2022? That’s a sign of high correlation and insufficient diversification.

- Target low-correlation additions: Based on your audit, identify gaps. If you hold only U.S. stocks, consider adding international equities, a commodity ETF (tracking gold or oil), or short-term Treasury notes. The cross-asset approach has a documented track record of improving risk-adjusted returns.

- Set target allocations: Define what percentage of your portfolio should go to each asset class. A simple starting point for a balanced investor might be 50% equities (split between U.S. and international), 25% fixed income, 15% commodities, and 10% alternatives.

- Implement gradually: You don’t need to restructure everything at once. Add diversifying assets over several months to reduce timing risk.

- Schedule regular rebalancing: Markets move, and your allocations drift. Reviewing and rebalancing at least annually maintains your target risk profile and forces disciplined buying of underperforming assets and trimming of overperforming ones.

Common mistakes to watch for:

- Overdiversification: Holding 50 equity funds that all track similar large-cap indices gives the appearance of diversification with none of the real benefit. You’ve just added costs.

- Underdiversification: Holding four individual tech stocks and calling it a portfolio. You’re exposed to a single sector’s fate.

- Ignoring alternative assets: Gold, oil, and Treasury bonds aren’t exotic. They’re foundational tools for maximizing risk-adjusted returns in 2026 and managing downturns.

- Neglecting monitoring: Setting up a diversified portfolio and ignoring it for years leads to silent drift. ETF market alerts can help you stay informed when allocations move significantly.

Pro Tip: Rebalancing doesn’t have to mean selling winners and paying taxes unnecessarily. You can rebalance by directing new contributions toward underweighted assets, keeping your tax bill lower while improving your allocation over time.

Why most investors get diversification wrong (and how to do better)

Here’s the uncomfortable truth that most investment content glosses over: owning more funds does not equal real diversification. We see this pattern constantly. An investor holds a U.S. large-cap fund, a U.S. growth fund, a technology sector ETF, and a NASDAQ-focused fund. They believe they have four diversified holdings. In reality, they have four slightly different versions of the same risk. The correlations between these funds are probably above 0.90, meaning they move almost in lockstep.

True diversification requires understanding what you actually own, not just how many funds or positions are on your statement. When you look under the hood of a typical “diversified” equity portfolio, you often find the same mega-cap names (Apple, Microsoft, Nvidia, Amazon) appearing in every fund. That’s not diversification. That’s concentration with extra fees.

Geographic and sector concentration risk is equally underestimated. Investors often feel safer with international exposure, but European and U.S. equity markets have become increasingly correlated over the past two decades as capital flows globally. Just adding a global equity index to a U.S. equity portfolio provides less risk reduction than it once did. The real diversifiers, the ones that actually changed the math, are assets like gold, oil, and government bonds that operate in fundamentally different economic environments.

The cross-asset portfolio data tells a clear story: mixing equities with commodities and Treasuries delivers higher Sharpe ratios than stock-only approaches. Yet most retail portfolios still consist almost entirely of equities, because that’s what’s marketed most aggressively and what feels most familiar.

Our view is that successful diversification is an ongoing practice, not a one-time setup. It requires periodically asking “what are the correlations between my holdings today?” not just “how many different things do I own?” Using a market volatility checklist as part of your regular review process keeps you grounded in the actual numbers rather than assumptions. The investors who outperform over decades aren’t the ones with the most holdings. They’re the ones who understand exactly what risks they’re carrying and why.

Track, diversify, and manage your investments with Handy.Markets

Smart diversification only works when you can see your whole portfolio clearly and respond quickly when markets shift. Knowing that gold just jumped 3% or that Treasury yields spiked matters in real time, not days later.

Handy.Markets gives you a single place to track all financial markets, from equities and commodities to Forex and crypto, with live prices and percentage changes across asset classes. You can set up free price alerts through Telegram, Discord, Slack, SMS, Email, or Webhook, so critical movements reach you instantly on the channel you already use. When it’s time to review your allocations or spot rebalancing opportunities, explore the ETF tools to find diversification options across markets in one place. Staying informed is the first step to staying diversified.

FAQ

What is the main goal of portfolio diversification?

The main goal is to reduce risk and smooth returns by holding different assets that don’t all move in the same direction. Low correlations between assets are what make this risk reduction mathematically possible.

Does more diversification always mean lower risk?

Not necessarily. True diversification depends on low correlations, not just a higher number of holdings. Assets with correlation below 1 reduce portfolio volatility, but adding highly correlated assets only adds costs and complexity without real protection.

How does cross-asset diversification compare to single-asset investing?

Mixing stocks, commodities, and Treasuries has meaningfully outperformed stock-only portfolios since 2009. Cross-asset portfolios combining the S&P 500, gold, oil, and T-notes show higher Sharpe ratios, meaning better return for each unit of risk taken.

How often should I rebalance my diversified portfolio?

Most investors review and rebalance at least annually to keep allocations aligned with their target risk profile. More active investors may rebalance when any single asset class drifts more than 5% from its target weight.

Recommended

- Top Investment Strategies To Maximize Returns In 2026 | Handy.Markets

- Market Volatility Checklist: Strategies For Traders | Handy.Markets

- Mastering Market Trends: 13% Annual Returns Proven Strategy | Handy.Markets

- Key Stock Market Trends Driving Investment Moves In 2026 | Handy.Markets

- How to Diversify Trading Strategies for Better Performance