TL;DR:

- Accurate financial asset tracking supports optimal investment decisions and long-term wealth growth.

- Using simple, consistent methods and tools like Empower or spreadsheets ensures reliable, manageable monitoring.

Financial asset tracking is the process of systematically recording, monitoring, and analyzing your financial holdings to support investment decisions and long-term financial planning. Whether you manage a personal portfolio of stocks and ETFs or run a small business with retirement accounts and equity compensation, knowing exactly what you own, what it’s worth, and how it’s performing is the foundation of every smart financial decision. This guide walks you through the tools, setup steps, best practices, and analysis techniques you need to build a tracking system that actually works, starting today.

What is a financial asset tracking guide and why does it matter?

A financial asset tracking guide is a structured framework for cataloging, monitoring, and reviewing every asset you hold, from brokerage accounts and retirement funds to real estate and cryptocurrency. The industry term for the broader practice is portfolio management, and tracking is its operational backbone. Without it, you are making investment decisions based on memory and guesswork rather than data.

Net worth equals assets minus liabilities, and this single number is a more reliable indicator of financial health than income alone. That means your tracking system needs to capture both sides of the ledger, not just the assets that feel good to look at. For small business owners especially, this means including liabilities like loans and credit lines alongside investments, retirement accounts, and equity compensation.

The stakes are real. Cost basis errors, missed rebalancing opportunities, and untracked liabilities can silently erode wealth over years. A well-built tracking system prevents all three.

What tools do you need to start tracking financial assets?

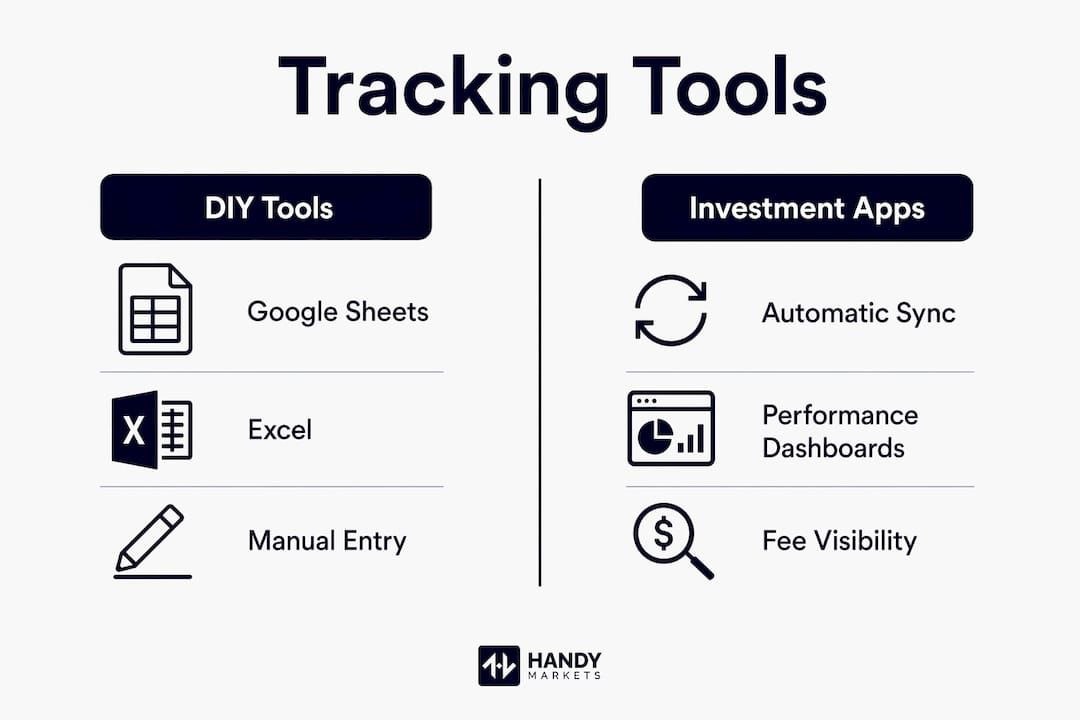

The right tool depends on your complexity level, your comfort with technology, and how much automation you want. The four main categories are spreadsheets, budgeting apps, dedicated investment trackers, and net worth aggregators.

![]()

| Tool Type | Best For | Automation Support | Key Limitation |

|---|---|---|---|

| Google Sheets / Excel | DIY builders, full control | Manual or API-based | Requires setup time |

| Empower (free) | Portfolio + net worth view | Auto-syncs accounts | Limited customization |

| Budgeting apps | Cash flow + asset overview | Moderate | Weak on investment detail |

| Net worth aggregators | Holistic financial picture | High | Privacy considerations |

Investment tracking apps that provide asset allocation views, performance dashboards, and fee visibility are preferred by most active investors, with Empower rated as the top free option for 2026. The reason is simple: tools that auto-download transactions and balances save hours of manual entry and reduce the risk of input errors.

Manual tracking in Google Sheets remains a strong choice for anyone who wants complete control. Manual entry fields typically include ticker symbol, quantity, current value, acquired date, and cost basis method, each of which directly affects how gains are calculated and reported. Spreadsheets also allow you to build custom dashboards, apply conditional formatting, and connect to financial APIs for semi-automated updates.

Pro Tip: If you are just starting out, begin with a free net worth aggregator like Empower to get a complete picture quickly, then layer in a spreadsheet for assets the aggregator cannot capture, such as private equity or real estate.

How do you set up a financial asset tracking system step by step?

Building a tracking system from scratch feels overwhelming until you break it into a repeatable sequence. Effective net worth tracking requires a clear target number, scheduled reviews, simple tools, automation where possible, and incremental improvements over time. Start simple and add complexity only when you need it.

Here is a proven setup sequence:

- Define your tracking goals. Decide what you are measuring: net worth growth, investment performance, retirement readiness, or all three. Your goal determines which data points matter most.

- Categorize your assets. Group holdings into buckets: taxable brokerage accounts, tax-advantaged accounts (401k, IRA), real estate, business equity, cash, and alternative assets like crypto. Small business owners should also include equity compensation and liabilities for a complete picture.

- Input your data. For each holding, record the ticker symbol or asset name, quantity, purchase date, purchase price, and cost basis method. This data is the foundation of every calculation downstream.

- Choose your update frequency. Daily updates suit active traders. Weekly or monthly updates work well for long-term investors. The key is consistency, not frequency.

- Set up automation where possible. A practical DIY pattern schedules daily data fetches that pull balances and transactions, transform the data, and append it to a spreadsheet with deduplication to prevent duplicate records. These workflows can execute in under 10 seconds, supporting near-real-time dashboards.

- Schedule regular reviews. Block time monthly for a full reconciliation and quarterly for a deeper portfolio review. Weekly spot checks take five minutes and catch errors early.

- Iterate and improve. After 90 days, identify what is missing or broken in your system and fix one thing at a time.

Handling complex assets requires extra care. Real estate valuations should be updated quarterly using tools like Zillow or a professional appraisal, not daily price feeds. Equity compensation, including restricted stock units and stock options, needs separate tracking for vesting schedules and tax events. Multiple brokerage accounts should be consolidated into a single view to avoid blind spots in your allocation analysis.

Pro Tip: Use a dedicated tab in your spreadsheet for liabilities and update it every time you make a significant payment or take on new debt. Net worth calculations are only accurate when liabilities are as current as your asset values.

What are best practices and common pitfalls in tracking assets accurately?

Accuracy in asset tracking is not a one-time setup task. It is an ongoing discipline, and the gaps tend to appear in predictable places.

Best practices to follow:

- Record cost basis at the time of purchase, not retroactively. Cost basis methods like FIFO and Specific Identification produce meaningfully different tax outcomes, and choosing the right one early gives you strategic flexibility at tax time.

- Reconcile your tracker against official brokerage statements monthly or quarterly. Regular statement verification reduces the risk of errors that accumulate silently over time.

- Use idempotent automation pipelines. Rerunning sync jobs without deduplication by transaction ID inflates your historical data permanently, making performance calculations unreliable.

- Preserve historical snapshots before making major changes to your tracker. This creates an audit trail you will thank yourself for during tax season.

Common mistakes to avoid:

- Overvaluing illiquid assets like private business interests or collectibles based on optimistic estimates rather than verifiable market data.

- Ignoring liabilities entirely, which produces a distorted net worth figure and a false sense of financial security.

- Relying exclusively on connected accounts for cost basis data. Cost basis can silently diverge after account transfers or corporate actions, and connected apps rarely flag this automatically.

- Updating inconsistently, which makes trend analysis meaningless because you are comparing apples to oranges across time periods.

“The biggest tracking error is not a calculation mistake. It is the habit of updating only when markets are up, which introduces survivorship bias into your own financial history.”

Specific Identification is the most tax-efficient cost basis method for investors who hold multiple lots of the same security at different prices. It lets you choose exactly which shares to sell, which can minimize capital gains in a given year. Setting this up correctly from the start, rather than defaulting to FIFO, is one of the highest-value decisions you can make in your tracking system.

How can tracked data drive smarter financial decisions?

Tracking data is only valuable when you use it. Raw numbers in a spreadsheet do not improve your finances. Interpreted numbers, reviewed on a schedule, do.

The most direct application is asset allocation analysis. Once you know the current value of every holding, you can calculate what percentage of your portfolio sits in equities, bonds, real estate, cash, and alternatives. Comparing that breakdown against your target allocation tells you exactly when and how to rebalance. Tools like Empower display this visually with charts and retirement readiness projections, making the analysis accessible even for beginners.

A few high-impact ways to use your tracked data:

- Performance benchmarking. Compare your portfolio’s return against a relevant index like the S&P 500 or a blended benchmark. This tells you whether your active decisions are adding value or whether a low-cost index fund would serve you better. You can explore smarter index investing to understand how indices function as benchmarks.

- Fee analysis. Aggregate the expense ratios across all your funds. A 1% difference in annual fees compounds dramatically over 20 years. Tracking makes this visible.

- Tax planning. Knowing your unrealized gains and losses by lot allows you to harvest losses strategically before year-end, offsetting gains elsewhere in your portfolio. This is where Specific Identification cost basis pays off most directly.

- Net worth trend analysis. Plotting net worth monthly over one to three years reveals whether your financial trajectory is improving, stagnating, or declining. This single chart is more motivating and informative than any monthly budget review.

For small business owners, tracked data also supports decisions about when to draw from business accounts, how to time equity compensation sales, and whether personal and business finances are properly separated. Reviewing top investment strategies alongside your tracked data helps you align your portfolio with your actual financial goals rather than generic advice.

Key takeaways

Consistent, accurate financial asset tracking is the single most reliable foundation for investment performance, tax efficiency, and long-term wealth growth.

| Point | Details |

|---|---|

| Start with net worth | Track assets minus liabilities from day one for a complete financial picture. |

| Choose tools by complexity | Use Empower for automation and Google Sheets for full control over custom data. |

| Record cost basis immediately | Choosing FIFO or Specific Identification at purchase time prevents costly tax surprises later. |

| Automate with deduplication | Idempotent sync pipelines prevent inflated transaction histories that corrupt performance data. |

| Review on a fixed schedule | Monthly reconciliation against statements catches errors before they compound over time. |

Why simple and consistent beats perfect and complex

At Handy, we have seen hundreds of investors abandon sophisticated tracking systems within three months because the maintenance burden outpaced the benefit. The pattern is consistent: someone builds an elaborate multi-tab spreadsheet with API connections, conditional formatting, and automated charts, then stops updating it the moment life gets busy. Six months later, the data is stale and the system is useless.

The tracking systems that actually improve financial outcomes are boring. They are a single spreadsheet updated every Sunday, or a free aggregator checked once a month, combined with a quarterly deep review. The tool matters far less than the habit.

One thing we feel strongly about: integrate cost basis tracking from the very first trade. Most people treat it as a tax-season problem and scramble to reconstruct purchase prices from old statements. That scramble costs money, both in time and in suboptimal tax decisions. Specific Identification requires lot-level records, and you cannot reconstruct those retroactively with confidence.

We also recommend treating automation as a supplement to manual review, not a replacement for it. Connected accounts are convenient, but they introduce silent errors after transfers, corporate actions, and broker migrations. A 15-minute monthly check against your official statements is the difference between a tracking system you can trust and one that merely looks trustworthy.

Start simple. Stay consistent. Add complexity only when a specific gap in your current system is costing you money or time. That is the approach that compounds.

Track your assets in real time with Handy.Markets

Once your tracking system is in place, the next challenge is staying informed when markets move. A well-organized spreadsheet tells you where you stand today. Real-time alerts tell you when to act.

Handy makes it easy to monitor live prices across stocks, ETFs, and crypto in one place, with no complex setup required. You can set up free price alerts across Telegram, Discord, Slack, SMS, Email, and Webhook in minutes, so you never miss a critical move in the assets you are actively tracking. Whether you are watching a stock approach a rebalancing threshold or monitoring a cryptocurrency position, Handy delivers the signal exactly where you need it. Start with one alert and build from there.

FAQ

What is financial asset tracking?

Financial asset tracking is the systematic process of recording, monitoring, and analyzing all financial holdings, including stocks, ETFs, retirement accounts, and real estate, to support investment decisions and financial planning.

What is the best free tool for tracking financial assets?

Empower is rated the top free investment tracking app for 2026, offering automatic account syncing, asset allocation views, performance dashboards, and retirement readiness calculations in one platform.

How does cost basis affect asset tracking?

Cost basis methods like FIFO and Specific Identification directly determine your taxable gains when you sell an asset. Recording cost basis accurately at the time of purchase is critical for both tax efficiency and performance measurement.

How often should I update my financial asset tracker?

Long-term investors benefit from monthly updates and quarterly deep reviews. Active traders may need daily or weekly updates. The most important factor is consistency, not frequency.

Can I automate my financial asset tracking?

Yes. Tools like the Plaid API combined with Google Sheets allow automated daily data fetches that run in under 10 seconds. Effective automation pipelines use deduplication by transaction ID to prevent duplicate records from corrupting your financial history.